Updated December 11, 2023

Form 943 is an IRS document filed once a year by agricultural employers to report federal payroll taxes withheld from their farmworkers’ wages. Federal payroll taxes include income tax and the employer and employees’ FICA contributions to social security and Medicare.

IRS Definition of “Farm”

The term ‘farm’ includes stock, dairy, poultry, fruit, fur-bearing animal, and truck farms, as well as plantations, ranches, nurseries, ranges, greenhouses or other similar structures used primarily for the raising of agricultural or horticultural commodities, and orchards.[1]

Table of Contents |

What is Form 943?

Form 943 is an annual federal tax return used by agricultural employers who pay taxable wages to their employees for farm labor.

Similar to Form 941 or Form 944, which are federal tax returns for non-agricultural employers, it reports the total amount of federal income tax and FICA tax contributions withheld from employees’ paychecks.

2024 FICA Tax Rates

Social Security: 6.2% each for the employee and the employer, with a maximum wage limit of $168,600.[2]

Medicare: 1.45% each for the employer and the employee. For individual wages that exceed $200,000 a year, the employer must withhold an additional 0.9% for additional Medicare tax.[3]

Who Files Form 943?

Any employer who paid wages to one or more farmworkers must file Form 943 if:[4]

- The employer paid a single employee cash wages of $150 or more in a year for farmwork; or

- The employer paid its agricultural employees a combined amount of $2,500 or more in wages (cash and non-cash) in a year for farmwork.

Note: Compensation paid under an H2-A visa (Temporary Agricultural Employment of Foreign Workers) is not subject to federal payroll taxes.

When is Form 943 Due?

Employers must file the form by January 31 following the tax year. If deposits have already been made in full payment of the taxes due, Form 943 can be filed by February 10.[5]

Where to File

Electronically

The IRS recommends filing Form 943 electronically. To e-file Form 943, use IRS-approved software to complete and submit the return. You may also use an authorized e-file provider to file it on your behalf. A fee may be charged to file electronically.

Where to Mail

If filing by paper, the mailing address for the return depends on whether a tax payment is included with Form 943.[6]

| States | Without a Payment | With a Payment |

|---|---|---|

| Connecticut, Delaware, District of Columbia, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin | Department of the Treasury

Internal Revenue Service Kansas City, MO 64999-0005 |

Internal Revenue Service

P.O. Box 806532 Cincinnati, OH 45280-6532 |

| Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming | Department of the Treasury

Internal Revenue Service Ogden, UT 84201-0005 |

Internal Revenue Service

P.O. Box 932100 Louisville, KY 40293-2100 |

| No legal residence or principal place of business in any state |

Internal Revenue Service

P.O. Box 409101 Ogden, UT 84409 |

Internal Revenue Service

P.O. Box 932100 Louisville, KY 40293-2100 |

| Special filing address for exempt organizations; federal, state, and local governmental entities; and Indian tribal governmental entities, regardless of location |

Department of the Treasury

Internal Revenue Service Ogden, UT 84201-0005 |

Internal Revenue Service

P.O. Box 932100 Louisville, KY 40293-2100 |

Instructions for Form 943 (10 Parts)

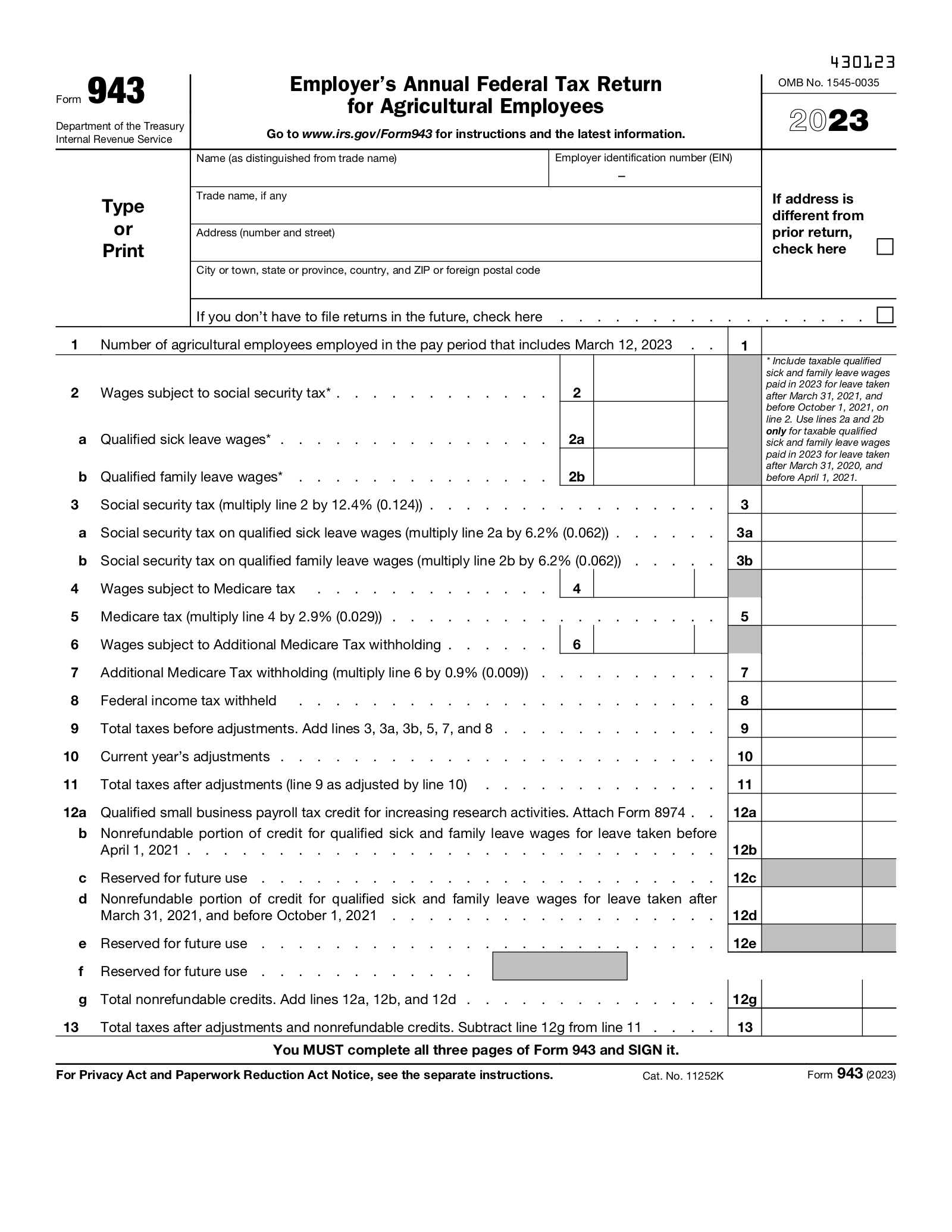

- Lines 1-9: Calculate Taxes Due Before Adjustments

- Lines 10-13: Calculate Taxes Due After Adjustments and Non-Refundable Credits

- Lines 14a-14j: Fill Out Total Deposits and Refundable Credits

- Line 15: Calculate Total Balance Due

- Line 16: Indicate Overpayment If Any

- Line 17: Complete Monthly Summary of Federal Tax Liability

- Lines 18-29: Indicate Qualified Health Plan Expenses and Sick Leave Wages

- Third-Party Designee

- Signature

- Form 943-V: Payment Voucher

Lines 1-9: Calculate Taxes Due Before Adjustments

To calculate your taxes due before adjustments, provide the following answers:

- Number of agricultural employees

- Wages subject to social security tax

- Qualified sick or family leave wages if any

- Wages subject to Medicare tax

- Additional Medicare tax withholding

- Federal income tax withheld

Lines 10-13: Calculate Taxes Due After Adjustments and Non-Refundable Credits

Adjustments are used to:[7]

- Round the fractions of cents; or

- Adjust for the uncollected employee share of social security and Medicare taxes on third-party sick pay or group-term life insurance premiums paid for former employees.

For lines 12a-12g, complete only if you have non-refundable credits to report for qualified small business payroll tax credit or qualified sick and family leave wages in 2021.

Lines 14a-14j: Provide Total Deposit Amount and Refundable Credits

Enter your deposits made for the year, including any overpayment applied from a previous year. Indicate the specific amounts.

Only complete line 14d if qualified sick leave wages or family leave wages were paid in 2022 for leave taken between March 31, 2020 and April 1, 2021.

Similarly, only complete 14f if qualified sick leave wages or family leave wages were paid in 2022 for leave taken between March 1, 2021 and October 1, 2021.

Line 17: Complete Monthly Summary of Federal Tax Liability

Only complete this section if you are a monthly schedule depositor. If you are a semi-weekly depositor, complete Form 943-A instead.

If your amount on line 13 (total taxes after adjustments and nonrefundable credits) is less than $2,500, do not complete line 17 or Form 943-A.

Third-Party Designee

Indicate whether you want to designate a third party, such as an employee or a tax preparer, to discuss the return with the IRS. If yes, provide the designee’s name, phone number, and PIN.

The third-party designee may:[8]

- Provide the IRS with any information that is missing from the return

- Contact the IRS for information about processing the return

- Respond to certain IRS notices about errors

Signature

An authorized signee must sign their full name, along with their official title. They must also provide a daytime contact phone number and the date.

The person authorized to sign the return varies depending on the type of business:[9]

- Sole proprietorship — The owner of the business.

- Corporation (including an LLC treated as a corporation) —The president, vice president, or other principal officer duly authorized to sign.

- Partnership (including an LLC treated as a partnership) or unincorporated organization — A responsible and duly authorized partner, member, or officer having knowledge of its affairs.

- Single-member LLC treated as a disregarded entity for federal income tax purposes — The owner of the LLC or a principal officer duly authorized to sign.

- Trust or estate —The fiduciary.

Form 943 may also be signed by an agent of the taxpayer authorized by a valid power of attorney.

Form 943-V: Payment Voucher

Complete this section only if you are making a payment along with your Form 943. You may only make a payment using the voucher if:

- Your total taxes after adjustments and nonrefundable credits for the year (line 13) are less than $2,500 and you’re paying in full with a timely filed return; or

- You’re a monthly schedule depositor making a payment in accordance with the Accuracy of Deposits Rule. In this case, the payment amount may be $2,500 or more.

Otherwise, tax deposits must be made via electronic funds transfer.

Frequently Asked Questions (FAQs)

What’s the difference between Form 941 and Form 943?

While both forms are federal tax returns used by employers, Form 943 is specifically for taxable wages paid for farm labor. In addition, Form 941 is filed quarterly (every three months) while Form 943 is filed annually.

Can Form 943 be amended after filing?

Yes. File Form 943-X to correct any errors made on Form 943. If making adjustments to more than one year, file a separate Form 943-X for each year.

Do Form 943 filers pay FUTA tax?

Yes — however, FUTA tax is not reported on Form 943. Use Form 940 instead to report annual contributions to federal unemployment tax.

Sources

- IRS — Publication 51 (2023), (Circular A), Agricultural Employer’s Tax Guide: Who are Employees?

- Social Security Administration: “Social Security Announces 3.2 Percent Benefit Increase for 2024”

- IRS — Topic No. 751, Social Security and Medicare Withholding Rates

- IRS — Instructions for Form 943 (2022): Who Must File?

- IRS — Instructions for Form 943 (2022): When Must You File?

- IRS — Instructions for Form 943 (2022): Where Should You File?

- IRS — Instructions for Form 943 (2022): Line 10

- IRS — Instructions for Form 943 (2022): Third-Party Designee

- IRS — Instructions for Form 943 (2022): Who Must Sign