Introduction

The transition point between higher education and entry-level accounting posts has been the focus of much previous research in determining the development of required knowledge, skills, and abilities (Albrecht & Sack, 2000; Bui & Porter, 2010; Lawson et al., 2014; Pincus et al., 2017; Thompson, 2013). This study begins with a novel and neglected transition point for accountants: from accountancy firm-based roles to industry-based roles, accountancy firms being typically where college-graduated students enter training contracts with such firms and industry being all non-accounting firm organisations. The historic, and rising, number of accountants transitioning to industry-based roles (IAASA, 2021; Mumford, 1991) accentuates the need to understand this process. Accounting education research has focused much less on accounting education offered by the professional bodies (M. Byrne & Flood, 2003), giving rise to calls for more research into the skills and competencies required of industry as accountants transition (Lawson et al., 2014; Rebele & St. Pierre, 2015).

The concept of career transition is one that has attracted attention across multiple disciplines (Guan et al., 2019; Sullivan & Al Ariss, 2021), with transitioning becoming a more prevalent phenomenon (Chudzikowski, 2012). A career transition is viewed here as a “changing role” as opposed to a “changing orientation to a role” (Louis, 1980, p. 30). Research on career transition has, for example, included sports athletes (Wylleman et al., 2004), nurses (D. Edwards et al., 2015), military personnel (Ghosh et al., 2019), architects (Sang et al., 2009), and moves from the academic to the work environment (Donald et al., 2018; Grosemans et al., 2017). This study focuses on the career transitions of accountants and extends beyond previous accounting studies that focus on transitioning of students to entry-level positions (Asonitou & Hassall, 2019; Holt et al., 2017; Oussii & Klibi, 2017; Sidaway et al., 2013). In particular, the study seeks to investigate accountants’ career transition from early career employment in accountancy firms to careers in industry.

This transition entails a process of socialisation in a new work setting (Ashforth & Saks, 1996; Morrison, 2002). It is a “process by which an individual comes to appreciate the values, abilities, expected behaviours, and social knowledge” required to enact a role and participate in an organisation (Louis, 1980, pp. 229–230); and one in which the “experiences of individuals in transition” are organised by members of the organisation transitioned to (Van Maanen & Schein, 1979, p. 230). Socialisation, also referred to as ‘onboarding’ (Klein & Polin, 2012), plays a role in helping organisations convey their culture to newcomers (Bauer et al., 1998) and helps them to adjust to a new work setting (Ashforth et al., 2007). Such processes, for example in the context of graduates transitioning to accountancy firms, include recruitment and selection, assessment of performance, training, mentoring, and career induction (McManus & Subramaniam, 2014; Simms & Zapatero, 2012). The need to study transition is driven by the rising frequency of job movements (Bauer et al., 2007) and the potentially long-term impacts that result from these transitions and socialisation processes (Bauer et al., 1998).

The study was motivated by a number of factors. Firstly, it seeks to develop on existing theory (Corley & Gioia, 2011; Edmondson & McManus, 2007; Ridder, 2017; Snow et al., 2003) relating to the phases of career transition (Nicholson, 1987) and combines the concepts of person–job fit (Chuang et al., 2016; J. R. Edwards, 1991; Kristof-Brown, 2000) and person–culture fit (Nazir, 2005; O’Reilly et al., 1991; Westerman & Yamamura, 2006) pertaining to transition. Secondly, to the authors’ knowledge, previously published research has not addressed this particular career transition, with the exception of some research on the transition of graduates into entry-level posts in accountancy firms (Anderson-Gough et al., 1998). Thirdly, the career transition literature has observed the very challenging nature of career transitioning for individuals (O’Brien‐Pallas et al., 2006) and for organisations.

The paper next presents the review of literature and the theoretical underpinnings to the study; this is followed by the research methodology. The findings are then presented using a thematic approach, which leads to a discussion of the implications of the findings. Some concluding remarks complete the paper.

Literature Review

Significant debate has taken place since the mid-1980s in relation to the failings of training and education to provide the skills and competencies required of accountants in the workplace (Albrecht & Sack, 2000; Brewer et al., 2014; Bui & Porter, 2010; Lawson et al., 2014; Siegel et al., 2010; Tatikonda & Savchenko, 2010; Thompson, 2013). Surveys from the US, Europe, and Australia have identified a range of important skills for accountants. These include problem-solving, communication, business awareness, IT skills, and generally emphasising gaps in non-technical aspects, such as interpersonal and team skills (Albrecht & Sack, 2000; Arquero Montano et al., 2001; Cory & Pruske, 2012; Dolce et al., 2020; Hassall et al., 2005; Kavanagh & Drennan, 2008; W. Richardson, 2005). Skills gaps continue to be observed in accounting education studies including areas such as IT, tax and audit, and accounting fundamentals (Daff, 2021; Edeigba, 2022; Kwarteng & Mensah, 2022). Parham et al. (2012) found a ‘silo effect’ in that a survey of US students’ future skills perceptions were narrowly defined within accounting and lowly ranked other business functions and wider economic matters. These studies have not addressed the skills relevant to accountants who transition from practice-based roles to industry-based ones. Qualitative research, in a European context, has found such industry-based management accounting roles to be diverse and challenging (S. Byrne & Pierce, 2007; Goretzki et al., 2013; Morales & Lambert, 2013; Windeck et al., 2015).

Studies to date have focused on the correspondence of skills developed in higher education with the requirements of practice-based accountants (Flood & Wilson, 2009; Pan & Perera, 2012; Stanley, 2013). Limited research exists in relation to accounting education offered by the professional bodies (M. Byrne & Flood, 2003), such as Chartered Accountants Ireland (CAI), and continuing professional development (CPD) providers (De Lange et al., 2013, 2015; Lindsay, 2016), in relation to the requirements of industry-based roles. This has resulted in calls for research into the skills and competencies required of industry (Lawson et al., 2014; Rebele & St. Pierre, 2015). Furthermore, in terms of accounting skills development and education research, much research has been predominantly based in North America, the United Kingdom (UK), continental Europe, and Australia (Coady et al., 2018; Hassall et al., 2005; Howieson et al., 2014) and broadening geographical perspectives are needed to contribute to the field of study.

The accountancy profession in Ireland has traditionally focused on audit and practice-based requirements, which is not surprising as auditing has been the core business of the profession for most of the twentieth century. CAI is the largest ‘recognised accountancy body’ (RAB) in Ireland, accounting for almost 50% of all qualified accountants (IAASA, 2021), with members employed in both practice and industry. As the requirements of the profession evolve, the traditional role of industry-based accountants as a scorekeeper is no longer viable. Accountants in industry now require myriad skills encompassing technical, professional, lifelong learning, and emotional intelligence skills drawing from survey research by Coady et al. (2018) and Jackling and De Lange (2009) in a Canadian and Australian context, respectively. This raises the issue of whether newly qualified CAs entering industry-based roles possess the skills required for their new roles. The call for a focus on industry is justified given that over 57% of qualified CAs are ultimately employed in industry (IAASA, 2021). Furthermore, the number of CAs employed in industry increased by 80% from 2008 to 2021 (IAASA, 2008, 2021) whilst, in contrast, the number of practice-based CAs grew by 55% during the same period (IAASA, 2008, 2021).

To understand this issue, it is necessary to understand the CA’s typical route to professional membership in an Irish context (Flood & Wilson, 2009), i.e. complete a higher education programme, then prepare for CAI’s final admitting examination (FAE) whilst simultaneously gaining mandatory professional training within an accountancy firm. It is acknowledged that in Ireland the majority of CAs train within practice (IAASA, 2021) but ultimately transition to industry-based roles within a year or two post qualification (Farmar, 2013). Whilst this study focuses on those with audit practice training backgrounds, it is acknowledged that some CAs do train in other settings, e.g. large tax, corporate finance, and consultancy professional practice firms as well as in more accounting-focused roles in smaller professional practice firms. Some CAs also train in industry, the public sector, and non-profits, often via the ‘Flexible Route’. It can be argued that whilst audit training provides a good foundation, there may be further development requirements with skills gaps requiring remediation upon entering industry. Additionally, a move from practice to industry involves moving from a training firm with arguably like-minded, similarly aged individuals in audit practice cultures (Hood & Koberg, 1991) to a new environment that can vary in size, culture, and in terms of the level of practical supports provided. Moving into a new organisation has been acknowledged as a stressful period from interview-based research on accounting placements in an Australian context (Stanley, 2013). In the case of CAs moving from practice to industry, there is a change in both the organisation and the role, which results in an even more challenging transition. An investigation of this transition of the CA from practice to industry is therefore warranted based on the argument that: 1) CA training is predominantly performed through practice-based firms; 2) most CAs will make the transition from practice to industry within a year or two post qualification (Farmar, 2013); and 3) the transition involves both the challenge of a change in role and a change of employer.

Research on transition is mainly in the human resources literature and has largely focused on school-to-work transitions (Fenwick, 2013; Swanson & Fouad, 1999), early-career socialisation (Ashforth & Saks, 1996), and promotion (Ibarra, 1999). Early-career socialisation, which has also been referred to as ‘onboarding’ in the literature (Bauer et al., 2007), encapsulates the various processes underpinning the assimilation of newly arrived employees into an organisation (Bauer, 2010; Cable et al., 2013; Gibson et al., 2003; Klein et al., 2015; Van Maanen & Schein, 1979). Nicholson and West (1989, p. 182) describe career transition as “any major change in work role requirements or work context” and Heppner (1998) expands on this definition suggesting career transitions occur when either a task change, position change, or occupation change is undertaken. It can be argued that the transition of a CA from practice to industry may encompass all three of these changes. The CA changes role from being an auditor, in many cases, to myriad differing titles and roles in industry. The tasks and skills in the new role are less likely to be audit focused and the CA must face the technical, organisational, and cultural challenges that a new organisation brings.

Empirically, this study adds to the extant literature on the skills needed for accountants transitioning from practice-firm roles to industry-based roles, which has not been previously researched. Theoretically, transition, and person–job fit and person–culture fit provide the lenses that frame the study and these are discussed in the next section.

Theoretical Underpinnings

From a theoretical perspective, the lenses employed in this study are Nicholson’s (1987) transition-cycle theory and fit theory, incorporating person–job fit (Kristof-Brown, 2000) and person–culture fit (J. R. Edwards, 1991). As a term seen in other qualitative studies of the accounting profession (Ahn & Jacobs, 2019; Sadler & Wessels, 2019; Verhoef & Samkin, 2017), the purpose of these theoretical lenses is to examine and understand the transition process relating to early-career accountants and as such underpins both the enquiry design and data analysis. These lenses are thus purposed in the vein of theory elaboration, beginning with theory and seeking “to understand how it needs to be altered to accommodate the data” (A. J. Richardson, 2018, p. 574). ‘Theory triangulation’ or ‘theoretical pluralism’ (Hoque et al., 2013, p. 1171) has been used previously in accounting studies (Ahrens & Chapman, 2006; Covaleski et al., 2003; Modell, 2005), whilst others have made observations on the under-deployment of theoretical frameworks in the area of accounting skills development (Coady et al., 2018; Haggis, 2009; McPhail, 2001; Tight, 2004).

Nicholson’s Transition Cycle Theory

Transitioning to new roles can have a substantial influence on individuals and organisations (Nicholson, 1987). Transition-cycle theory posits that such transitions go through a cycle of preparation, encounter, adjustment, and stabilisation (Nicholson, 1987). ‘Preparation’ describes the period before embarking on a new role. Nicholson and West (1989, p. 182) specified that the preparation phase is a “process of expectation and anticipation before changes”. This view of preparation confines it to the emotions of change without suggesting the need for practical research, formulating plans, and training in advance of the role change. In contrast, Drew-Sellers and Fogarty (2010) suggested that individuals should take charge of their own developmental trajectory when moving organisations and that preparation for a job transition provides the opportunity to take stock of developmental needs. ‘Encounter’ involves the early stages of the new role; as Van Maanen (1976) described, there is essentially a breaking in of new employees, and it can be a challenging experience (Ecclestone, 2009). The third stage in transition-cycle theory (Nicholson, 1987) is ‘adjustment’, which is concerned with identifying how to perform in the role and involves role development to minimise job misfit. Finally, ‘stabilisation’ assumes that the transition finally reaches a position of equilibrium. Nicholson’s (1987) transition-cycle theory, whilst nascent theoretically in accounting research, has been employed in other occupational settings, for example nursing (Carroll, 2004), mentoring (Hall & Chandler, 2007), and career expatriation to foreign countries (Nicholson & Imaizumi, 1993).

Nicholson’s transition-cycle theory is used as a lens through which the transition of the CA is viewed, as it sets out the potential phases of transition that must be traversed by CAs in the transition from accountancy firm-based roles to industry-based roles. Consistent with Nicholson’s theory, this transition involves both personal and role development. Personal development entails the CA adapting to fit the role through the development of skills, whilst role development involves the role adapting to fit the CA.

Person–Job Fit Theory

Studies of transition processes to work settings employ person–job fit theory (Chilton et al., 2010; Neuenschwander & Hofmann, 2021; Sortheix et al., 2015). The fit between individuals and their jobs has long been an area of interest for academics, employers, recruiters, job seekers, and incumbents (Kristof-Brown, 2000). Edwards (1991) described person–job fit as the fit between an individual’s abilities and the demands of their role. It is an important consideration in the recruitment and selection process (Werbel & Gilliland, 1999) and in the design of training interventions (Sutarjo, 2011). Higher levels of fit result in increased job satisfaction (Cable & DeRue, 2002), better role performance (Li & Hung, 2010; Wang et al., 2011), and reduced intentions to quit the organisation (Cable & DeRue, 2002; Wang et al., 2011). Chuang et al. (2016) expanded on the person–job fit concept arguing that it includes the dimension of skill; this fit concept is supported by Muchinsky and Monahan’s (1987) complementary-based view, which posits that an employee complements the characteristics of the workplace when their skills complement the requirements of the position. This dimension of skill within person–job fit can be extended to competency in that one may possess a particular skill, but competency considers whether such a skill has been effectively applied (Kristof-Brown & Guay, 2011). Boritz and Carnaghan (2003, p. 10) attribute the varying conceptualisations of competencies, in part, to the particular setting of interest. For example, educational settings tend to focus on skills that can be developed, while in an organisational recruitment setting there is less focus on development but more on the “screening for required or attractive attitudes and personality traits”. Thus, the former conceptualisation as skill development in the context of transition presents scope to examine the implications of job-fit for professional education and development.

Person–Culture Fit Theory

The culture of an organisation reflects “a pattern of shared basic assumptions” that has “worked well enough to be considered valid and, therefore, to be taught to new members” (Schein, 2010, p. 18). Person–culture fit has been identified as the “idea that organisations have cultures that are more or less attractive to certain types of individuals” (O’Reilly et al., 1991, p. 491) and thus individuals intentionally move in and out of organisations (Schneider, 1987). As a result, failure to align with culture may result in an employee vacating their position (Nazir, 2005; Wang et al., 2011; Westerman & Yamamura, 2006; Wheeler et al., 2007), which is an undesired outcome in any transition. Therefore, there is a need to consider person–job fit through the alignment of skills simultaneously with person–culture fit in the transition process. Studies have shown that recruits whose values align with those of the organisation adjust more quickly (Chatman, 1991), feel more satisfied (Chatman, 1991; Westerman & Yamamura, 2006), and intend to remain with the organisation longer (Chatman, 1991; Nazir, 2005; Westerman & Yamamura, 2006). Indeed, values are identified as the crux of person–culture fit, with Nazir (2005, p. 42) finding that “correlation between the organizational value profiles and the individual value profiles determines the person–culture fit”. Nazir (2005) further suggested that person–culture fit may provide insight into employee adjustment to a new organisation and as such, person–culture fit was determined as a lens that would provide insight into the adjustment of CAs transitioning from practice to industry.

Research Questions

Drawing upon the theoretical perspectives of career transition, person–job fit, and person–culture fit, and seeking to address the paucity of research relating to the CA transition process, an investigation of the transition of CAs from practice to industry is undertaken to help answer the following research questions:

RQ1: How do CAs experience transition from practice to industry?

RQ2: How do CAs develop the necessary skills and competencies to assist them in that transition?

RQ1 draws upon the theoretical perspectives of career transition (Nicholson, 1987) and person–job fit (J. R. Edwards, 1991) and person–culture fit (O’Reilly et al., 1991). The former maps the anticipated transition journey, whilst the latter identifies job and culture alignments on entering a new job in industry. RQ2 assesses the skill and competency requirement for CAs on transitioning and how such requirements might be best developed. To the authors’ knowledge, neither question has been addressed previously in published research, notwithstanding many CAs making this career transition (IAASA, 2021). The next section presents the research methodology and methods for the paper.

Research Methodology and Methods

This section details the qualitative design adopted in the study (Patton, 1990). Gaining a contextual understanding of the nature of the transition process experienced, and associated skill alignments and development, supported the use of a qualitative design (Flick et al., 2004; Savin-Baden & Major, 2013). To address the research questions, an interview-based approach was deemed most appropriate. Such an approach is merited when addressing questions of a ‘how’ nature and in seeking to attain some depth to the enquiry (Hennick et al., 2020; Yin, 2018). Following ethics committee approval, the data for this study were collected through semi-structured interviews as supported by their use in previous studies relating to accounting skills and competencies, and studies of early-career accountants (e.g. Anderson-Gough et al., 2001; Bui & Porter, 2010; Drew-Sellers & Fogarty, 2010). In the following sub-sections, we elaborate on the qualitative design elements of sampling strategy, the interview guide design, interviewee recruitment, and the data analysis process.

Sampling Strategy

The qualitative sampling strategy was a purposive one, driven by the research questions, and targeted “information-rich” interviewees (Patton, 1990, p. 169). We took a stakeholder sampling approach in targeting those most directly involved and those “who might otherwise be affected by it” (Palys, 2008, p. 697). Interviewee recruitment was via personal and professional chartered accountants’ networks and contacting the ‘Big 4’ (PwC, Deloitte, EY, and KMPG) and smaller accountancy firms. Table 1 describes the sample of interviewees who participated in the study, along with the criteria applied to interviewee selection and the participant reference key, e.g. CAs, etc. In common with the approach used by Bui and Porter (2010), the views of 28 stakeholders were sought. This involved seeking perspectives from newly qualified CAs for whom memories of transition were very current and from longer-qualified chartered accountants (LQs), who have benefited from the passage of time and deeper reflection. In addition, and in the context of a qualitative approach, of interest was how the transition was viewed from stakeholders involved at the other side of the hiring transaction, namely industry-based hiring managers (HMs), recruiters (RECs), and a CPD provider. Finally, the perspective of a representative of Chartered Accountants Ireland (INST) was considered valuable as both the regulator and representative body for those involved in the transition.

Interview Guide Design

The semi-structured interview guide, in relation to the CAs’ transition from practice to industry, was arranged according to sub-topic areas and informed by previous literature as illustrated in Table 2.

In the majority of cases, interviewees were asked about the sub-topic areas listed in Table 2, particularly if they were qualified accountants with knowledge of both industry and practice and had transitioned themselves. If interviewees did not have transition experience, the area of transition (sub-topic area 2) was not discussed. An information sheet and consent form were used as part of the interviewee recruitment process.

Interviewee Recruitment

A full profile of the interviewees, which includes contextual descriptive data relating to the interviewees and the reference key used in the presentation of the quotations in this paper, is provided in Table 3. Of the 28 interviews, 17 were conducted in person, with 11 conducted by telephone. One interviewee was located in the UK, having trained in Ireland. All the remaining interviewees were located on the island of Ireland: four in Northern Ireland and 23 in the Republic of Ireland. All interviews were recorded.

Data Analysis

Data analysis was based on Braun and Clarke’s (2006, pp. 87–88) six-step approach: “familiarisation with the data, generating initial codes, searching for themes, reviewing and defining themes, and finally producing the findings”. These six stages were iteratively used through the data analysis phase. The qualitative analysis software package NVivo was used as a tool to aid in the analysis process and improve the rigour of the data review (Richards & Richards, 1994). The use of the memo tool in NVivo aided in producing reflexive work and allowed a clear audit trail that can provide evidence of a systematic, iterative, and multi-faceted approach to the qualitative data analysis (Houghton et al., 2016). Memos also acted as mechanisms for self-reflection regarding the researcher’s role in the research process – as a professional accountant interviewing another professional accountant – to ensure biases were recognised and minimised (Bulpitt & Martin, 2010; Onwuegbuzie, 2003). Recording in memos made preconceptions explicit and thus heightened awareness of them.

Applying Braun and Clarke’s (2006) six steps commenced with immersion in the data through many transcript readings (step 1: familiarisation) that then led on to the creation of codes (step 2). The reading and coding process was iterative and recursive in reviewing and revising codes as appropriate. Appendix 1 provides an illustration of these codes at the end of the hierarchical paths displayed. The coding was based upon insights from the literature review (e.g. theories of fit and transition, skill requirements) and acted as a reflective prompt against the researcher’s professional practice knowledge and experience of the research topic as a chartered accountant in context. Abstracting to a higher level from these codes (step 3: searching for themes), themes were identified from the created list of codes, effectively grouping related coded segments of text into higher-level themes). Reflection during the coding process led to some codes being merged, whilst others were further refined or their higher-level thematic classifications were further evaluated. Step 4 (reviewing themes) involved evaluating these created themes and making refinements as required (as indicated by the labelling in Appendix 1 towards the beginning of the hierarchical path). Step 5 (defining and naming themes) examined the final labelling and describing of themes to reflect their “essence” (Braun & Clarke, 2006, p. 92). Step 6 (producing the report) then involved cycles of writing up, to detail the analysis process, using quotations for “thick description”, and to give an “account of the story the data tell” (Braun & Clarke, 2006, p. 93). The following section discusses the findings of each theme in more detail.

Findings

A number of themes emerged from the data analysis namely: fit with role and culture (Theme 1); practice to industry transition phases (Theme 2); skills gap (Theme 3); and supports in developing competency in skills required for industry (Theme 4). Themes 1 and 2 on fit and transition phases address Research Question 1 and Themes 3 and 4 on skills gap and development address Research Question 2. This section offers an analysis of these themes.

Theme 1 – Fit with Role and Culture

A frequently emerging theme in the findings was the alignment of CAs’ skills with their roles, in conjunction with the cultures of their respective organisations. Person–job misfit is a problem that exists, but it is one that could be addressed. As HM1 remarked:

“I think the clear thing is to look at the job role that the person is coming into and to identify their existing skill set versus what you need. You would ideally hope that they would have a lot of what you need and you would put training in place, be that a combination of in-house and sending them on courses.”

Culture fit was perceived as more challenging. CA12 noted his experience:

“There is a number of elements about how the organisation goes about its business that I don’t enjoy … their worldview and their modus operandi isn’t in line with what I would consider is the best way to do things …”

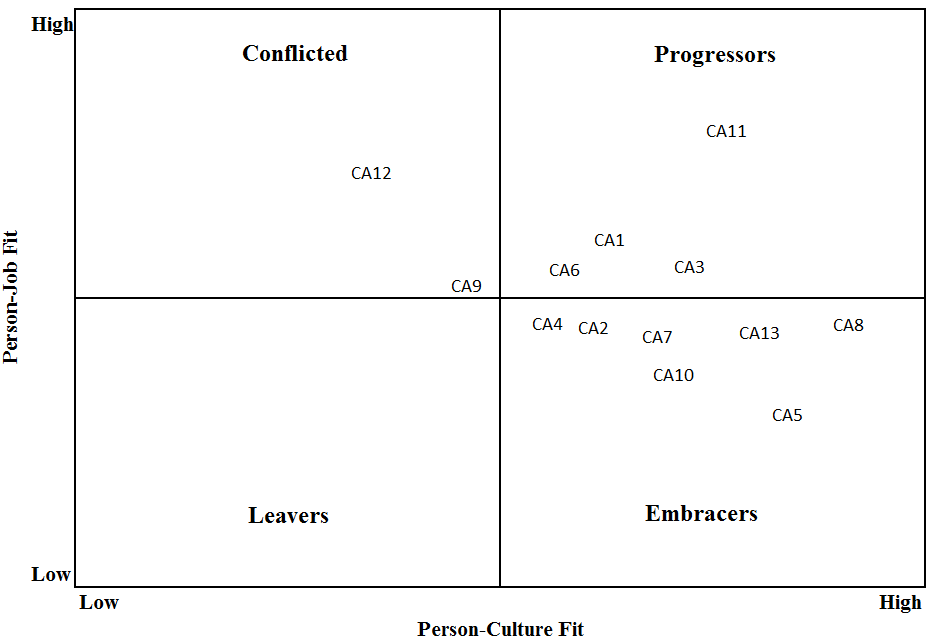

While a HM reflecting back on his experience as a transitioning CA, HM6 recalled: “I didn’t enjoy it from the cultural perspective … to be honest, I was there for a year and I couldn’t get out of it quick enough.” The evidence supports consideration of person-job fit and person-culture fit in the CA’s transition process. As HM6 commented: “it is very important that you get the role that fits you and the company culture that fits you”. This analysis of interview data led to the development of a fit matrix (see Figure 1) as a visualisation mechanism to assist interpretation (Nadin & Cassell, 2004) and to “condense more and more data into a more coherent understanding” (Miles & Huberman, 1994, p. 91). The interview transcripts were reviewed multiple times to gain perceptions of how the CAs interviewed aligned with the matrix and a judgement was made based on the data collected as to where the CA resides on the matrix. This matrix emerged from the data analysis phase of the research and whilst the very small qualitative sample size base to this matrix is duly noted, it seeks to offer an understanding of how the varied job and culture alignments of CAs might be positioned when considering job and culture fits as continua of high and low. Four categories of CAs in transition are designated as Leavers, Conflicted, Embracers, and Progressors.

High levels of culture and person fit are titled ‘Progressors’. In some cases, Progressors were those who had the benefit of previously auditing the company (i.e. CA1, CA3, and CA6), whilst in one other case, there was an individual who went into an internal audit function that aligned well with their practice training. Progressors included CA11, for example, who joined internal audit and had an agricultural background, joining an organisation in the agricultural sector:

“I am in internal audit so it is not that much of a transition but work hasn’t been that much different and was relatively easy to pick up, but it was a nice transition.”

Individuals with high levels of person–job fit, but with lower levels of person–culture fit, appeared to have doubts about whether to remain within their role and are thus termed ‘Conflicted’. CA12 stated that: “I think I am an excellent fit to the role, but I don’t think I am an excellent fit to the organisation.” CA9 also appeared conflicted stating: “I don’t know what the next step is for me.” Both of these CAs joined SMEs and a factor in this misalignment with culture may have been that they did not have the support of other professional accountants working in their organisations. The person–culture fit was emphasised by LQ3 who stated that “the culture was the main part” and REC2 who believed “if people aren’t enjoying a certain role, we usually find that it is due to the culture”.

CAs with higher levels of person–culture fit but with lower levels of person–job fit seemed to embrace learning their new role through the various supports provided and are therefore labelled ‘Embracers’. CA4 and CA13 commented:

“The culture is a lot less stressful which you know I think is good. It feels like they are trusting you to get your job done in the manner in which it needs to be done but I found there was a lot to learn but you were supported through this learning.”

“… the people I am dealing with here are much older and have much more experience, but they are great and don’t get so fazed by you if you make a mistake … I felt very aware of my own age and level of experience, as I am one of the youngest in the finance department. I guess it was to not hide when I didn’t know things because they can see through your bluff.”

There was evidence of many CAs being categorised as ‘Embracers’: those who were culturally aligned but in need of skill development. It was found that the majority of those interviewed were Embracers.

Finally, those who align neither with culture nor with job are destined to leave the organisation resulting in the quadrant labelled ‘Leavers’. Whilst there was no CA that fitted this category, HM2 did speak of letting “somebody go” due to misfit in both these dimensions. This quadrant is of interest to this study, but none of the CAs interviewed could be aligned here. This is perhaps due to the constraint of the sampling frame chosen, i.e. where CAs were qualified in practice no more than two years prior to the date of the interview and had transitioned to, and remained in, their first role in industry for at least three months. Furthermore, a larger sample would have offered more scope to research this.

Person–culture fit is based on a fit of company culture with an individual’s attributes and personality, which can be difficult to change, and which may result in CAs vacating their position, as CA12 and HM6 demonstrated. However, a lack of person–job fit is not considered to be insurmountable, as HM4 said: “my experience is that they [CAs] learn quickly, they have a very good work ethic and a willingness to learn”. Based on this observation, person–job misfit might be addressed with training and development interventions through the different phases of transitions, which is the second theme discussed in the following section.

Theme 2 – Practice to Industry Transition Phases

Many CAs had little awareness of industry roles in the preparation phase (Nicholson, 1987) of transition, as reflected in their initial perceptions: “surprised” (CA4) and “different” (CA3 and CA5). Ancillary CPD activities were not undertaken and there was little information available:

“I don’t think there is enough information out there” [INST].

“when I was coming out, you weren’t sure of even what type of roles there are out there” [LQ5].

“when you are in the Big 4 there is absolutely zero emphasis on what you can do after you leave the Big 4” [REC2].

A finding that was frequently articulated by many interviewees was the perceived differences between practice and industry roles, e.g. a broader age profile and fewer social interactions in the work environment, less emphasis on technical development versus experiential development, and less support than a trainee in practice. Those CAs who had either audited the company they joined, or those who had availed of secondments to the company, were better prepared.

In the encounter phase (Nicholson, 1987), the initial move was perceived as “challenging” (CA6 and CA7), “tough” (CA6), “daunting” (CA2), and “difficult” (CA1). Larger organisations afforded more time to CAs to settle in, whilst other HMs in smaller organisations expected CAs to get straight into their role from day one. CAs appear conditioned from their experiences in practice. Their prior experience ensures that they are highly professional in their approach to their new role, which helps in addressing person–job fit. However, this conditioning is tested when the CA transitions to a company that lacks like-minded individuals, and this observation suggests that there is a socialisation required of accountants when entering industry. Adjusting to culture as opposed to the job presented more challenges in this phase, e.g. CA12 could not adjust to the differences from their practice role that resulted in a clear intention to quit.

Nicholson’s (1987) adjustment phase was found to have two distinct sub-phases, grounding and assessing. For both CAs and HMs, the first sub-phase, “a good grounding” (CA1), was perceived as a bedding-in of the CA into both the role and culture of the organisation, as HM4 remarked: “getting used to the organisation, getting used to the systems and the processes”. Perceptions varied but it was generally perceived early in transition e.g. “the first three months” or “between three to six months, they are comfortable in doing what the previous person was doing” (HM4). LQ5 observed more the latter end of timing: “A lot of people go in and might give it a month or two months and say no it’s not for me and go off but I would say give it six months or a bit of time anyway.” It was found that this sub-phase was about gaining an understanding of the culture along with the vision, goals, and strategy of the organisation. This alignment to the culture of the organisation was found to be achieved through socialisation of the new employee by way of inductions and onboarding. The second, assessing sub-phase, related more to employer “expectations” (HM4, HM6) of the CA in seeking “to stretch them further” (HM1) and:

“… expecting them to own the role from there on and they don’t need that micromanagement … that they are familiar, and they are confident in the role then you know” [HM6].

These assessments sometimes resulted in the lengthening of the timeframe that it took to reach the next transition phase (CA9, CA11, and CA13).

The final stabilisation phase (Nicholson, 1987) was evident in CAs being comfortable in their roles and most perceived they had reached this phase:

“… definitely after the six-month period, there was definitely more stuff coming my way even in terms of helping out other units if people were a bit behind. I would start to get thrown stuff similar to how the rest of the team were” [LQ2].

Being in the role four months, CA12 appeared not to have reached a stabilisation phase and expressed an intention to quit due to the cultural challenges encountered. The period to the stabilisation phase varied, but appeared linked to the support provided to the CAs for skill development and to understand the complexities of the business and its culture.

Theme 3 – Skills Gap

It was found that a skills gap exists, which was acknowledged across all of the interview participant groups. There were clear differences between CA and HM perceptions of the skills requiring development for industry-based roles. The skills gap was evident in both the CAs’ lack of understanding of skill requirements and in HMs’ perceptions of a CA’s skills:

“Some of the skills that I needed, I may not even have known in a skills-based audit, so it is not until you are in the job maybe three, six, nine months that you realise oh I didn’t realise I needed this skill” [CA10].

“I don’t think we would recruit an individual from practice straight into a commercially focused management accounting role that is responsible for the delivery of our budget … it would be too much of a jump” [HM6].

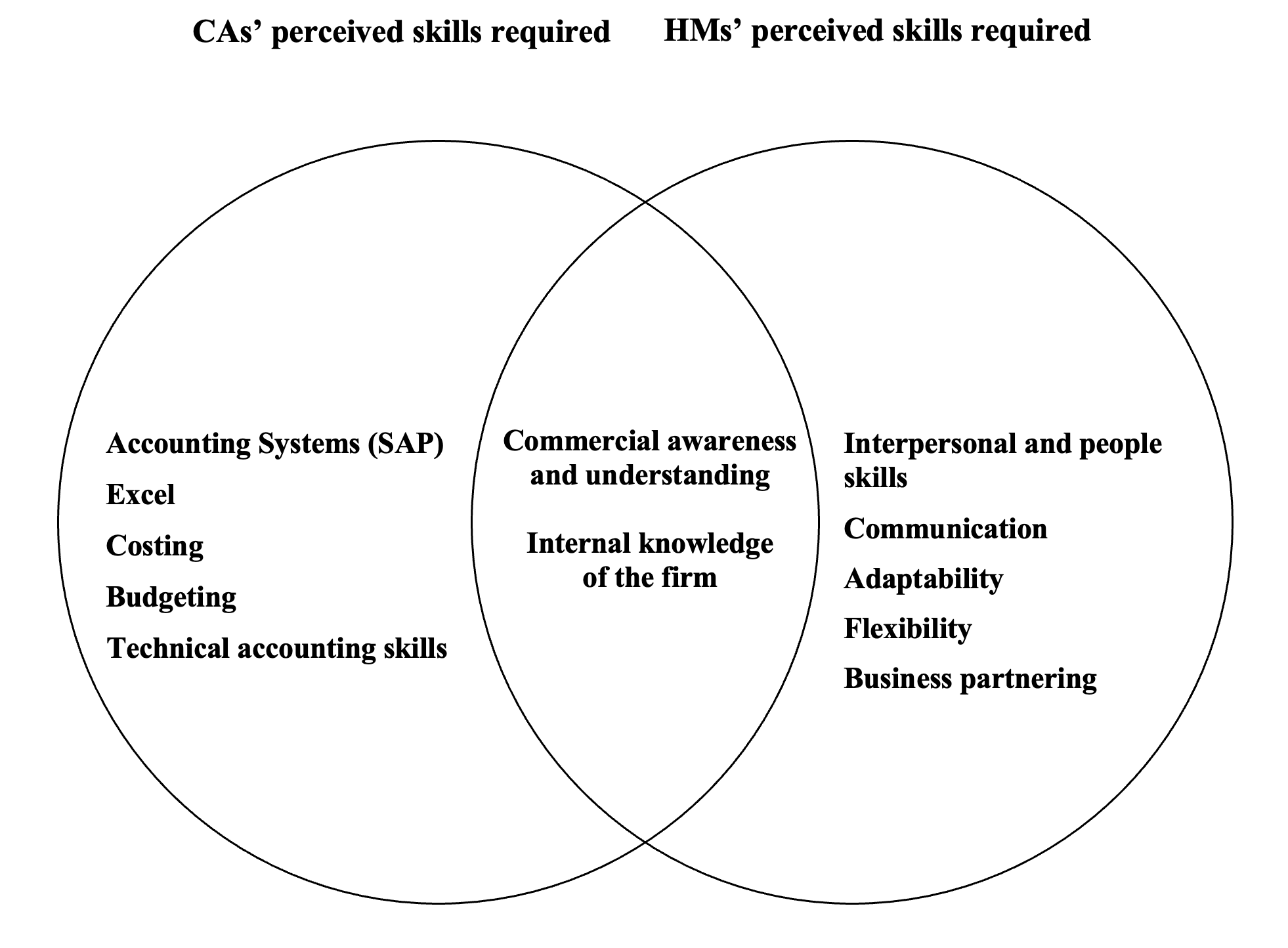

There is a focus by most CAs on the requirement for “hard skills” (CA10), “financial accounting around local GAAP” (CA12), software use and specific management accounting tasks such as costing and budgeting. In contrast to the CAs, HMs tend to focus on soft skills such as interpersonal skills, communication, business partnering (“move across the departments” (HM3)) and being adaptable and “flexible” (HM5) as highlighted in Figure 2. Both CAs and HMs shared perceptions of the need for “commercial awareness” (CA9) and an “understanding of the business” (HM4).

REC2 noted that CAs are “very weak on the double entry and the journal side of things”. LQ5 believed that “you can become a qualified chartered accountant and not know the first thing about putting a set of accounts together” with CA4 explaining that “your double entry when you are in the Big 4 is horrendous”. Others noted that the examinations “cover up understanding gaps” (CA12) as well as computerised systems (CPD) creating distance from fundamental accounting. INST perceived this as less of an issue for CAs coming from “a small to medium size” context but noted concern on these skills as “a lot more companies, particularly like your Americans are asking for it, for accounting tests as part of the interview process”.

This study found that CAs perceive using accounting systems such as SAP and associated software such as Excel as skills requiring development. This is somewhat surprising given that younger generations are often thought to be more proficient in adapting to new forms of information technology. These alternative HM and CA skill perceptions are interesting and it is posited that CAs in the first instance are focused on addressing the technical job requirements and, perhaps, this is less visible to the HMs.

Having identified the more significant skills gaps that exist, albeit there is some discrepancy between the interviewee cohorts, the next theme of the research looked at the supports required to help alleviate some of these gaps.

Theme 4 – Supports in Developing Competency in Skills Required for Industry

The findings revealed a number of aspects to supports for CAs in transition including induction, networks, in-house support, CAI training, CPD training, and mentoring.

CAs transitioning to SMEs were often expected to find their own way, whilst larger companies tended to afford the CA an induction period and the allocation of a “buddy system” (LQ2). In a multinational organisation context, HM6 noted:

“… it was a full five-day induction programme and it was an introduction to [Company Name], what the company is about, what our products are, what are our key departments …”

CA12, in an SME context and being in the organisation for four months, commented: “I thought the onboarding process was minimal”. Similarly, CA8 noted, “you are pushed in at the deep end”. In contrast to these smaller organisation settings, onboarding in larger organisations entailed a more structured approach to meeting organisational leaders, more formal communications around the company’s mission, values, strategies, and the provision of some context in relation to the people dynamics of the company.

Many CAs utilised their own peer networks as important supports to transition: individuals who were also going through a similar process. CAs also networked with prior work colleagues in particular in the preparation and encounter transition phases.

“The people from [practice firm] were the greatest support that I have had in my career” [CA9].

The necessity of this networking support may mean that those coming from smaller practices may not always have an appropriately sized network.

The provision of ongoing in-house support was found to be one of the most frequently mentioned support mechanisms provided by employers. This involved first, arranging meetings with key stakeholders and internal customers of that role, and second, providing an opportunity to sit next to someone within the organisation who took them through the tasks of that role.

“My mom and dad still work in the business so yeah you are always talking about it” [CA8].

“I guess the VP was pretty helpful” [CA13].

It was found that these supports were more informal, unstructured, and ad-hoc in smaller organisations and this was a challenge to some CAs who were coming from a very structured and supportive practice background.

Whilst some CAs perceived CAI professional examination training as “brilliant” (HM3), “the foundation” (LQ1) and “applicable to industry … especially in management accounting” (CA9), it was found that many of those interviewed believed that CAI professional examination training should be directed more towards the needs of industry:

“Not great. It is very practice-focused. It is extremely practice focused” [CA13].

“I felt it was definitely geared towards those who are going to be staying in practice” [LQ2].

Whilst interviewees acknowledged CAI’s introduction of a competency-based framework involving a multidisciplinary case study approach in examinations, and more electives (CAI, 2018), some suggested that CAI training could provide more focus on industry requirements. Given the previous training in practice, more information on industries, companies, and roles was frequently mentioned by interviewees.

It was found that CAs struggled to manage their own CPD upon transition due in part perhaps to this being managed previously by training firms. CA12 remarked: “I haven’t done formal CPD during the year” (CA12). CAs observed limited guidance on CPD (although the CAI might dispute this) and many CAs and LQs called for CAI to offer some form of CPD training in relation to transition:

“It really would be helpful, like even to understand the difference between financial accounting and financial analysts, group accountant, an SG&A analyst, business analyst, like they are so different but to the untrained ear they are just an accountant in industry” [CA13].

“… people coming in, to actually explain what they do and what their experience has been” [CA8].

Mentoring was not perceived as a support in transition. As CA1 remarked: “I wouldn’t say there was one.” HM3 noted that “people don’t want mentors”. CA9 remarked that:

“… there could be a bit more support from Chartered Accountants Ireland on the mentoring side and also being more informative for people in making that transition” [CA9].

CAs seemed unfamiliar with mentoring and remarked about some informal internal coaching in the previous practice environment, and that it was either absent or less structured in industry:

“I am in the real world here and there is nobody looking after me” [CA9].

“I would go and sit with her for a half hour or an hour and go through things” [CA11].

Whilst CAI does offer a mentoring service to all members, it appears that CAs do not avail of this support. This is consistent with the CAs being poorly prepared, as noted earlier, for the transition process and unaware of the supports to assist in this challenging period. Perhaps one explanation for this could be that their prior practice-based experience was very much in-house supported and that kind of strong developmental support was not available in the same way in industry.

In undertaking this study, a range of experiences from a variety of perspectives were shared. These were distilled into the four themes that formed the basis of the analysis and these are discussed next.

Discussion

The findings support the importance of person–job fit (Chuang et al., 2016; Kristof, 1996; Wang et al., 2011) and person-culture fit (Chatman, 1991; Kristof-Brown & Guay, 2011; O’Reilly et al., 1991; Westerman & Yamamura, 2006), with the latter being identified as more challenging to address. The integration of these fits led to the development of a tentative framework of transition quadrants labelled as Leavers, Conflicted, Embracers, and Progressors. Progressors knew that they would fit the culture and they were also more aligned to the role due to the knowledge of the business that they already possessed (Chatman, 1991; Nazir, 2005; O’Reilly et al., 1991). Consequently, they had higher levels of person–culture fit (Westerman & Yamamura, 2006) and person–job fit. Furthermore, many of these interviewees joined companies with other like-minded and similarly trained professionals already in place (Schneider, 1987), which aided in the alignment of shared values. Conflicted CAs had higher levels of person–job fit but lower levels of person–culture fit that prompted questioning of their future with their current employers (Wheeler et al., 2007). This resulted in less congruency between their values and those of the organisation and impacted upon their socialisation within their respective organisations (O’Reilly et al., 1991). Embracers, the quadrant pertaining to most CAs in the study, had higher levels of person-culture fit but lower levels of person–job fit. Whilst there has been little analysis of the initial roles of CAs in industry, there have been a large number of studies analysing management accounting roles which suggests industry-based roles can be varied and complex (S. Byrne & Pierce, 2007; Goretzki et al., 2013; Maas & Matějka, 2009; Morales & Lambert, 2013; Windeck et al., 2015). This aligns with the identification of the need for many CAs to develop skills specifically required of industry. CAs characterised as Leavers align well neither with the culture nor with the job. Whilst none of the transitioning CAs were depicted as such, there is still the possibility, and there was evidence from HM2 that this had occurred.

The high frequency of interviewee discussion regarding fit with the organisational culture suggests that socialisation is of importance to transitioning CAs. This is consistent with Gibson et al. (2003) who suggested that individuals are more aware of the socialisation process when they change jobs or organisations. There is some limited research in relation to addressing cultural gaps (Nazir, 2005) following the hiring process with Gibson et al. (2003) offering that the most effective way of changing values is through impacts upon behaviour. It would seem that where person–culture misfit occurs, there is an incentive for the employer to support the socialisation of the CA that ensures the CA remains with the company longer (Chatman, 1991; Nazir, 2005; Westerman & Yamamura, 2006). This study found that this socialisation effort could be achieved through the employer offering inductions, onboarding supports, and buddy systems.

The concept of person–job fit is traditionally viewed as the basis for employee selection (Werbel & Gilliland, 1999). In some cases, HMs have accepted that CAs that have been categorised as Embracers will have a certain level of misfit upon entering roles in industry. However, prior experience in practice appeared to mitigate gaps that exist upon entering industry, ensuring better role performance (Wang et al., 2011) and reducing intentions to quit the organisation (Cable & DeRue, 2002; Wang et al., 2011). This study found that person–job misfit is surmountable in CA transitions and, consistent with Sutarjo’s (2011) recommendations, may be addressed through training and development interventions through the different phases of transitions.

The study observed CAs passing through five phases within the process of transitioning from accounting practice-based roles to industry-based roles. These observed phases support Nicholson’s (1987) four phases (preparation, encounter, adjustment, and stabilisation) depicted in transition cycle theory but with some further empirical elaboration evident in Nicholson’s penultimate adjustment phase. Regarding the first transition stage of preparation, it was found that many CAs were not well informed on their future industry roles. The second encounter phase was evident in the initial period of the CA’s role in industry as it was challenging for the majority of interviewees, supporting previous research (Ecclestone, 2009; Louis, 1980; Stanley, 2013). It was found that Nicholson’s third adjustment phase (Nicholson, 1987) could be elaborated into two distinct sub-phases termed grounding and assessing, being a bedding-in process and an evaluation process, respectively. The final stabilisation stage (Nicholson, 1987) was in evidence for CAs albeit with differing timescales.

An observed CA–employer skills gap is consistent with the findings of Brewer et al. (2014), Siegel et al. (2010), and Tatikonda and Savchenko (2010), who all argue that US accounting education is practice-oriented despite almost two-thirds of US accounting graduates being employed in industry (Siegel et al., 2010). In an Irish context, CAI is influenced by the ‘Big 4’ practice firms (M. Byrne & Flood, 2003), which recruit the vast majority of trainee chartered accountants. Such firms have an orientation to the training needs of practice and not industry whilst acknowledging they fund such training. This does, however, underscore some skill deficiencies and when over half of qualified CAs in Ireland soon move to industry (Farmar, 2013), it indicates the need to understand how to best address this throughout the transition phases (Bauer, 2010). It was found that both CAs and HMs perceived commercial awareness and understanding along with internal knowledge of the organisation to be important for further development, consistent with the findings of Dolce et al. (2020) and Kavanagh and Drennan (2008). CAs also focused on the hard skills of management accounting such as costing and budgeting, which they would not have been exposed to in practice, but which are of importance in industry-based roles (Siegel et al., 2010; Tatikonda & Savchenko, 2010). Findings were consistent with Cory and Pruske (2012) who found that entry-level non-public accountants perceived Microsoft Excel as the most important skill required of new accounting graduates. In contrast, HMs do not identify IT skills as important and, again, this is consistent with the literature, with Arquero Montano et al. (2001) finding that employers do not view IT skills as a high priority as they perceive that students at both entry-level and newly qualified levels are proficient in this area. Similarly, Dolce et al. (2020) observed employers placing less emphasis on IT skills. Consistent with the findings of this research, Hassall et al. (2005) went further, suggesting that IT skills are no longer a priority to employers and resources would be better utilised to aid the development of softer skills. However, very recent research has shown employers emphasising IT skills (Kwarteng & Mensah, 2022). Several stakeholders highlighted a deficiency in fundamental accounting skills for CAs coming from larger accounting firms. These basic accounting skills were recognised by Kavanagh and Drennan (2008) as one of the top three skills valued most by employers and it is therefore very surprising that this study found that some CAs are perceived as lacking in this area.

The findings indicated a range of supports that are needed to develop the skills of CAs for industry-based roles. Whilst inductions can help CAs to adapt to their new environments, it is accepted that onboarding plays an important role in helping to socialise these new employees (Klein et al., 2015; Morrison, 2002). The mandate to enhance inductions for entry-level public accounting careers (Simms & Zapatero, 2012) could be extended to enhance career inductions of post-qualified accountants who transition from practice-based roles to industry-based roles. CAs were found to utilise networks of peers: those similarly experiencing transition and, to a lesser extent, prior practice work colleagues, consistent with Drew-Sellers and Fogarty (2010), who identified that early career management accountants understand that social networks are valuable resources.

The provision of ongoing in-house support was evident, consistent with Klein et al. (2015). The findings indicated that the CAI professional examinations could be more industry-oriented, supporting the findings of Brewer et al. (2014) and Siegel et al. (2010) in the US higher education context. As the majority of CAs are ultimately industry-employed (IAASA, 2021), it is in the interest of CAI to provide information on different industry career opportunities to entry-level CAs (Sidaway et al., 2013) in the transition preparation stage.

CAs were found to have not engaged much in CPD activities upon transition. This has implications for CAs regarding lifelong learning, career development, and adaptability (De Lange et al., 2013, 2015; Lindsay, 2016). It is surprising that the CAs did not take greater control over their continuous learning, as Kavanagh and Drennan (2008) have found that accounting students rate continuous learning as the most important skill for their future careers. Perhaps one explanation for CAs’ perspectives on continuous learning differing from those of students in higher education is that CAs’ perspectives may have been shaped through their subsequent years of professional education and experience. CAs’ views differ to those of students in higher education. Mentoring played little part in the transitioning process, notwithstanding its recognition as an aid to the onboarding of entry-level accountants (McManus & Subramaniam, 2014). The findings suggest CAs lack awareness of the mentoring and CPD provisions that could support their transition processes.

Conclusions

This study set out to understand how CAs experience transitioning from practice to industry and develop the necessary skills and competencies to assist them in that transition. The study provides the following contributions.

Firstly, the study presents a fit matrix (see Figure 1) as a useful tool to aid our understanding of the transition from a person–job fit and person–culture fit perspective. The identification of the fit matrix provides the means to a better understanding of the job and culture fit dimensions of the transitioning CA. The findings support the importance of person–job fit and person–culture fit (Kristof-Brown & Guay, 2011; O’Reilly et al., 1991) and the emergence of these in the data collected supports the need to consider both fits to assess the new employees’ transition. Therefore, this study suggests the simultaneous consideration of both person–job fit and person–culture fit as the existence of one fit without the other may limit positive transition outcomes and can lead to an employee vacating their position.

Secondly, in relation to Nicholson’s transition cycle theory, the study offers an additional nuancing of one of the phases of transition: the phase titled by Nicholson as the “adjustment phase” (Nicholson, 1987). Whilst the phases of transition were closely aligned to Nicholson’s theory, the findings suggest that Nicholson’s adjustment phase has two sub-phases of grounding and assessing, and this finding offers an extension to the theory. The grounding sub-phase was found to be about understanding the basics of the role and gaining an understanding of the organisational culture, along with the vision, goals, and strategy of the organisation. During the assessment sub-phase, HMs were found to place expectations on CAs and an assessment of the CAs against these expectations was carried out. This finding supports Nicholson’s adjustment phase in showing an evolving job fit through the transition process but, whilst Nicholson’s theory focused on person–job fit (Nicholson & West, 1989), the findings of this study show that the CAs’ person–culture fit is also relevant at this point in the transition process.

Thirdly, the participants in the study highlighted that there were some skills in need of development as CAs moved from practice to industry. This was not unexpected as industry-based roles are very different to practice-based roles. However, of greater interest was that there were distinct differences between the skills perceived as important by the CAs and those perceived as important by the HMs. CAs believed that the skills most in need of development were hard skills such as in information technology, technical accounting, and management accounting, whereas HMs tended to focus on communication, interpersonal skills, and being adaptable and flexible. This finding runs counter to much reporting in the literature of there being an overemphasis on the technical versus broader skill development. It is proposed that a possible reason for these CA–HM differences in perception is that CAs, in the first instance, direct their efforts towards addressing the technical aspects of the new role, which might be less visible to the HMs, and once these challenges are overcome, the CAs then look towards developing the other skills required for a successful transition. The study therefore draws attention to the temporal aspects of skill development in transitioning to industry-based roles.

In making the transition from practice to industry a variety of stories were heard from those who had relatively smooth transitions to those who experienced very challenging times. There was a wide continuum of practices by employers towards supporting new hires into their organisations. From the limited sample size, it was found that the CAs considered structured inductions and ongoing training to be beneficial to the transition. Interestingly, the CAs relied heavily on their own peer group, many of whom would have been prior work colleagues whilst in practice and be at a similar stage in their careers. However, they did not make use of the CAI mentoring scheme, and many did not know of its existence. This perhaps reflects a lack of preparation prior to the decision to move away from practice. The lack of basic information and understanding of the transition by CAs has been highlighted earlier, where it was noted that CAs do very little to understand what the transition from practice to industry involves prior to making the decision to leave practice.

Whilst the focus of this study is at an early-career transition phase for CAs, it nevertheless has implications for higher education in how it sheds light on how accounting graduates move through their early CA careers and the lifelong perspective of student learning. For educators, in preparing accountants for future careers, attention needs to be given to career transitions and how such transitions can be challenging experiences, the variations that exist within particular organisational cultures, and accounting roles therein. Students preparing for CA careers need to be informed of the supports that are available for career transitions and those supports that they can themselves foster in various networks as they exit higher education. Regarding the accounting curricula, particular skill gaps indicated included areas such as fundamental accounting, management accounting, information systems, interpersonal skills, communication, adaptability, flexibility, and business partnering.

Recommendations, Limitations and Further Research

This study has a number of implications. CAs could, in advance of transitioning, anticipate a significant change of role, seek to better understand industry employer expectations, leverage networks, and avail of CPD or professional body supports. For HMs, there is scope to provide more structured support across the transition phases and to target soft skill development as CAs emphasised harder skills. The development of the fit matrix will be of interest to HMs for ensuring a successful transition and to reduce the time taken to reach the stabilisation phase. For CAI, further consideration of the skills and understanding required for CAs who transition to industry-based roles in the development of training and development programmes is merited.

It is acknowledged that this study is challenged by its qualitative nature. Whilst in an Irish context, it is contended that the findings may have some transferability (Lincoln & Guba, 1985) to other worldwide professional bodies such as the American Institute of Certified Public Accountants, the Institute of Chartered Accountants of England and Wales, the Institute of Chartered Accountants of Scotland, Chartered Accountants Australia and New Zealand, Certified Public Accountants, and the Association of Chartered Certified Accountants, which have members who take a similar career path. Positioning on the fit matrix was a qualitative assessment based upon the perceptions of the CAs of their respective fits with job and culture. As these constructs were not measured, there exists a limitation in terms of certainty of the placement of each CA upon the matrix and the small underlying sample size. The study involved a multiple stakeholder approach with CAs, LQs, HMs, a CPD provider, RECs and CAI all being interviewed. Whilst many voices were heard, the research may have benefited from perceptions from further stakeholders such as higher education institutes and practice-based firm managers.

It would be meaningful to extend this research to members of other professional accounting bodies that follow a similar pathway to accounting roles in industry. Many of the skills captured in the data would provide an initial step in identifying a profile of skills to support a survey instrument for a quantitative-based study that may offer a broader perspective of the range of skills required across different industrial sectors. The subject area would benefit from wider research, particularly from a longitudinal study, to better understand the transitional process as it evolves and unfolds. Future work could seek to develop the fit matrix with the inclusion of a larger sample of qualified CAs. There was some evidence that transition to a former audit client may be beneficial and further research could determine the differences between transitions to former audit clients versus those who do not transition to former audit clients.

In summary, this study extends our understanding of CAs in the transition process to industry from practice and provides insights into the CA’s person–job fit and person–culture fit, the phases of the transition process, a skills gap, and the range of transition supports. Given the lack of existing research and the volume of CAs experiencing these transitions, this research offers an initial understanding of the processes involved.